Over the past 25 years, our national debt has surged from approximately $5 trillion to around $36 trillion, and our annual budget has widened from a surplus of $180 million to deficit of nearly $2 trillion. It’s sobering to think that a quarter-century ago, we had a budget surplus, and now we’re facing a budget shortfall that is comprised of annual interest payments projected to reach between $1.5 trillion and $1.75 trillion this year. This should concern every American.

While I have tried to remain apolitical in my personal and professional outlook, it is clear to me that leaders from both political parties have mismanaged our country’s finances for the past 25 years, and with the current trajectory of adding $2 trillion to the national debt each year, we’re heading toward a dangerous debt spiral.

So, how do we address this?

The straightforward, albeit unpopular, answer is that the system requires an overhaul. However, as mentioned earlier, structural changes can be exceedingly painful, especially when the decision to change is made for us rather than by us.

In this quarterly Market Update, I’ll share our firm’s perspective on how the current administration’s efforts to structurally transform the U.S. economy may lead to a challenging economic environment if policies remain unchanged.

I’ve titled this letter “The Fall.”

For a detailed explanation, please visit the Different Investments website. Below is a summary of our analysis.

Summary Analysis:

Throughout history, we’ve seen superpowers rise and fall, each following a similar trajectory. While history doesn’t repeat itself exactly, it often rhymes.

In recent years, Ray Dalio, founder of Bridgewater Associates, has warned that the U.S. is on an unsustainable path. Without structural changes, the U.S. risks losing its superpower status, leading to a tumultuous decline. In his 2022 analysis, “The Changing World Order,” Dalio examines the rise and fall of major economies over the past 500 years. His evidence-based research paints a concerning picture for the U.S.

This isn’t new information. Our research over the past two years has consistently highlighted systemic issues affecting the average American. For instance, on November 30, 2023, I noted that the Federal Reserve might allow the unemployment rate to rise to 5.5% before addressing systemic economic problems (currently, it’s at 4.2%). In our March 1, 2024 letter, I discussed the challenges the U.S. faces with its debt at both consumer and government levels. Last October, I highlighted the disparity between the U.S. economy and the stock market that has persisted over the last 15 years, emphasizing that in recent years many Americans are struggling to make ends meet.

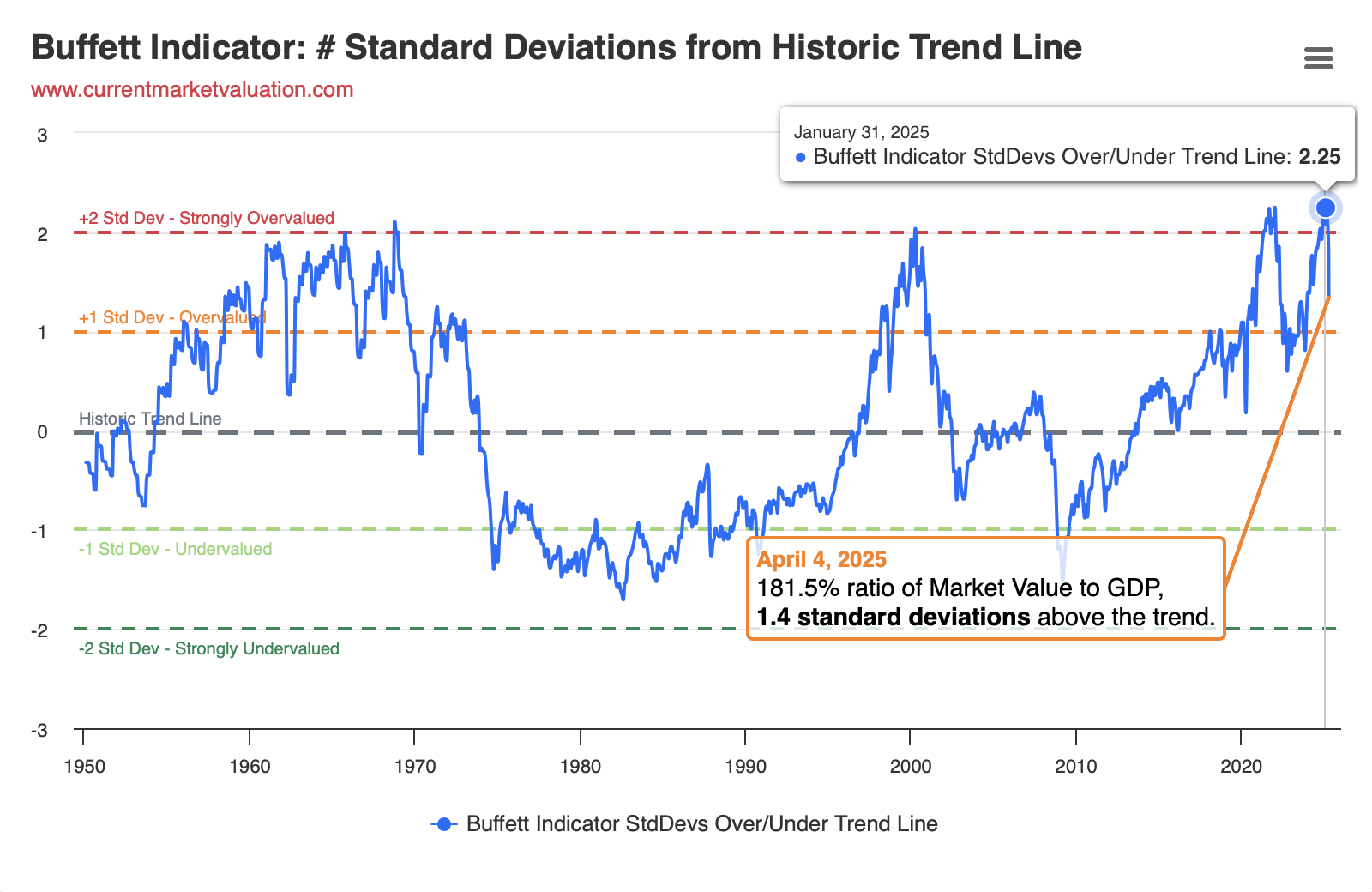

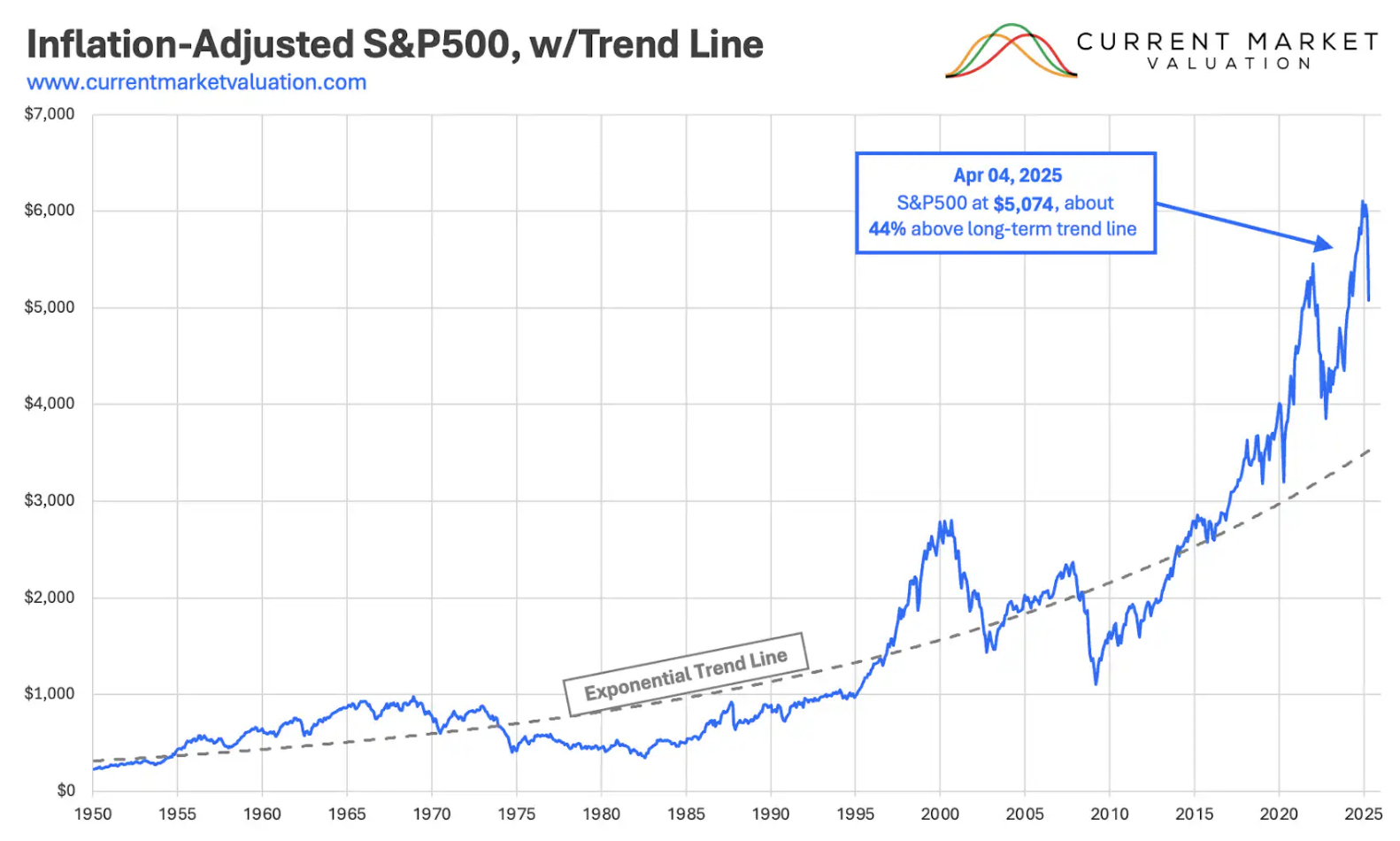

Nearly a year ago, on March 29, I shared a letter titled “Winter Is Not Coming, But Is A Recession?” In it, I pointed to historical indicators suggesting an impending recession. While my evidenced backed forecast may have been 12 to 18 months early, the signs were evident and have only worsened since. One indicator that continues to stand out is the “Buffett Indicator,” which stood at 225% on January 31, 2025. This is one reason that likely explains why Warren Buffett has sold a significant number of his investments within Berkshire Hathaway and now holds over $330 million in cash. After Friday’s close, the indicator has only fallen to 181%, implying there’s still considerable downside before reaching parity. For context, after the 2000 bubble burst, the S&P 500 fell below parity. In other words, if the S&P 500 were to revert to the 70-year trend line, we could see it drop to 3,500, or lower.

Over the past two years, we’ve invested across equity and fixed income markets while employing hedging strategies to protect against a sudden market downturn. Although these hedging positions have occasionally dragged on our investment strategies, I’ve remained steadfast in our thesis that the market is overvalued, systemic issues persist in the economy, Americans are struggling, and the mounting debt will eventually pose a significant problem. Enter 2025…

At the start of the year, during client Annual Reviews, I continued to express concerns about systemic problems and the first 100 days of the new administration. Specifically, I was apprehensive that the post-election rhetoric mirrored the “turnaround” playbook commonly used by new CEOs in failing companies. We’ve seen this with recent CEO changes at companies like Starbucks, Boeing, and Intel. Typically, these CEOs begin by slashing expenses to operate “lean.” If further cuts are needed, they proceed cautiously to avoid cutting too deeply. Once they’ve achieved their desired outcome, they focus on increasing revenues, often through product expansion or entering new markets. The current administration appears to be following a similar approach – cutting spending and seeking new revenue sources.

So, how have our portfolios fared, and what’s next for the markets?

The first question is easier to answer. As of Friday’s close, our strategies are positive for the year, and our hedging strategies have recovered losses from the past 12 months. After reducing equity exposure last September, we’ve experienced minimal equity loss while remaining strategically invested in short-term fixed income markets.

Predicting the market’s future is more uncertain, but our research indicates more pain ahead. For example, if tax cuts are expected to spur capital investments, the administration will need to offset this with spending cuts and increased revenue. With a goal to cut $1 trillion from the annual deficit (which could lead to significant layoffs) and raise between $300 billion to $600 billion annually from tariff policies, we’re entering a period of fiscal austerity. While this may help balance the budget, the dynamic between the President and the Federal Reserve Chair will be crucial in determining the economy’s fate. The President needs to reduce the debt’s interest expense to create a budget surplus, allowing for reinvestment in the country or paying down the national debt. Unfortunately, since tariffs are expected to increase annual core inflation by 1% to 2%, the Federal Reserve is once again battling inflation. This was underscored on Friday when Chair Powell stated, “Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.” Essentially, this means they cannot cut rates without risking entrenched higher inflation, as we’ve seen over the past five years.

As the world faces these challenges, our investment strategies remain defensively positioned. Should equity markets experience further downward pressure, our strategies are optimized for risk reduction, and portfolios with hedging strategies should see increased returns.

Detailed Analysis:

It’s incredible how much can change in just a few months. At the start of the year, we saw optimistic headlines like “The S&P 500 is forecast to return 10% in 2025.” Now, the narrative has shifted to concerns such as “US stock market loses $4 trillion in value as tariffs escalate.” Analysts are rapidly adjusting their forecasts, with median year-end projections for the S&P 500 dropping from 6,500 to the mid-5,000s. Market sentiment is turning sour, and it’s happening fast.

Based on our research, we believe these revised forecasts might still be overly optimistic. Three main factors contribute to this outlook: tariffs, stagflation, and the mounting U.S. debt. Let’s delve into each of these areas to understand the potential challenges ahead.

Tariffs

You’ve likely come across numerous articles discussing tariffs and their potential impact on the U.S. economy. What’s often overlooked, however, is how tariffs could play a strategic role in maintaining the U.S.’s position as a global superpower for the next half-century.

Historically, American leaders like Alexander Hamilton advocated for tariffs to protect budding industries from foreign competition. For instance, after the War of 1812, the U.S. implemented the Tariff of 1816 to support domestic manufacturers by making imported goods more expensive. This strategy continued post-Civil War, fostering industrial growth and job creation, though it also sparked debates about increased consumer costs.

Fast forward to 1948 and the introduction of the Marshall Plan. Officially known as the European Recovery Program, it aimed to aid Western Europe’s recovery after World War II with goals like economic revitalization, political stability, containing communism, and promoting international trade. While there wasn’t a formal agreement allowing foreign countries to impose tariffs on U.S. goods without reciprocation, the U.S. adopted a lenient stance toward European nations’ trade policies to support their rebuilding efforts. This leniency wasn’t meant to be permanent; as European economies strengthened, trade relationships were expected to become more reciprocal.

In recent decades, many manufacturing jobs have shifted overseas to take advantage of lower production costs. This migration has led to a decline in domestic factories and jobs, a shrinking middle class, and increased reliance on foreign goods. Events like the COVID-19 pandemic have highlighted the vulnerabilities of depending heavily on global supply chains – especially across critical industries like energy, pharmaceuticals, industrials, and materials.

Today, as artificial intelligence (AI) becomes integral to sectors like industrials, defense and energy, controlling the production of critical components is vital. Manufacturing critical component products domestically ensures they meet our standards and are readily available, bolstering national security and maintaining economic dominance.

In essence, while tariffs may pose short-term costs to U.S. consumers, they serve a strategic purpose. By rebuilding critical manufacturing infrastructure, we not only enhance national security but also position the U.S. as a leader in essential industries for the foreseeable future.

Stagflation

Stagflation – a period marked by stagnant economic growth, rising unemployment, and increasing inflation – is a challenging economic condition. It’s akin to facing multiple ailments simultaneously: a sluggish economy, job losses, and climbing prices. Tariffs can exacerbate stagflation by causing prices to rise quickly and potentially slowing the economy further as it undergoes structural shifts.

The pressing question is whether this structural shift could lead to a recession. While it’s difficult to assign exact probabilities, the risk is significant. For example, JPMorgan has recently increased their recession probability estimate from 40% to 60%, now considering a recession their “base case” for 2025.

With core inflation projected to rise to between 3.5% and 4.5% in the coming quarters and unemployment expected to increase gradually, the Federal Reserve faces a dilemma. Balancing its dual mandates of full employment and price stability becomes increasingly complex. If both inflation and unemployment deviate similarly from their targets, the Fed may adopt a “wait and see” approach, potentially leading to tensions between the Fed and the administration. This uncertainty could result in heightened market volatility as investors attempt to anticipate policy moves.

U.S. Debt

The growing national debt is a concern that could dampen economic and equity growth over the next decade. Analyses from institutions like Goldman Sachs, Vanguard, and Wells Fargo project average annual returns for the S&P 500 for the following decade to be between 2% and 6%, reflecting these challenges. However, in more extreme cases, some analysts are estimating S&P 500 returns could see an average annual return of negative 5%.

As of February 2025, interest payments on the national debt reached $395 billion, up from $350 billion during the same period in 2024. Annualized, this could exceed $1.8 trillion in interest payments this year. While increased tax revenues from tariffs might offset some of this burden, the primary way to reduce interest costs is by lowering the Federal Funds rate.

This situation sets the stage for a potential standoff between the Federal Reserve and the administration. If tariffs lead to higher prices and sluggish growth – hallmarks of stagflation – the Fed might hesitate to cut rates, keeping them between 4% and 4.25% longer than anticipated. This scenario forces the Treasury to refinance $9.2 trillion maturing in 2025 at these elevated rates.

To compel the Fed to lower rates, the administration might need to accept a recession, with rising unemployment and a contracting economy. Such conditions would likely prompt the Fed to cut rates to stimulate growth, subsequently reducing interest payments on the national debt. However, this strategy involves significant risks and could lead to increased market volatility as investors react to the unfolding economic landscape.

In summary, while the path ahead presents challenges, strategic use of tariffs and careful economic management could position the U.S. for long-term dominance in critical industries. Navigating the complexities of stagflation and managing the national debt will require coordinated efforts and may involve short-term sacrifices to achieve these long-term goals.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. You cannot invest directly in an index. Asset allocation is no guarantee of risk reduction. Past performance is no guarantee of future results.

{kind=link}

{kind=link}