Disclosure: The following article is not investment advice. Conduct your own research before making any changes to your investment strategy. Consult with your financial advisor before making portfolio changes… if you do not have a financial advisor click the link at the bottom of this article to complete a portfolio review with our team. Past performance is no guarantee of future results. You cannot invest directly in indices. Asset allocation may not result in portfolio risk reduction.

Before I dive in I want to draw a point of similarity to the 2000, 2001, and 2002 market decline – all led by the Nasdaq’s surge in the late 90’s. In looking at the stock market’s growth during 2021 & 2023 much of the increase was attributed to the Nasdaq, namely in 2023 by seven to ten stocks. If you scroll to the charts below you can see the markets remain above their respective 10 year average price channel (with the Small Cap market priced within its channel). Why is this important? I continue to remain worried about price action and S&P 500 earnings “reverting to the average”.

October’s overall performance was challenging to navigate. Technicals indicated October 3rd was the “bottom” of the market decline since July 19th. This is why I exited all of the short positions around S&P 500 4,225. It was my belief we would have short-term year end rally up to 4,550 (at the high side). Unfortunately, four days after I exited the short positions the war in the Middle East broke out. This contributed to a limited rally in the S&P 500 to 4,376 before turning negative and dropping below a major support level at 4,200.

The “last hope” to save the year-end rally fizzled out over the last 10 days with S&P 500 earnings solidly beating estimates, and yet the market shrugged off the good news. If that wasn’t good enough Q3 2023 GDP was reported at 4.9% indicating very strong economic growth. So what does this mean?

The Fed Chair Jerome Powell has recently stated the economy is too “hot”. In other words, the Fed is trying to slow the economy so core inflation continues its downward trend. Unfortunately, with initial jobless claims coming in lower than expected, job hires being higher than expected, and the unemployment rate remaining near historic lows Chair Powell continues to remain concerned inflation won’t come down fast enough since employees continue to have money to spend. The Board of Governors have stated they want to see below trend growth (0-2%) in order to know if their interest rate policy is working.

This leads me to maintain my mid-term negative view that the market is overvalued. Over the last 10 days I have rebalanced the fixed income positions in the Moderate Conservative and Moderate Aggressive along with a large portion of the equities across all investment strategies. I maintain allocations to defensive equities, a few key mega-tech companies, and a few stocks awaiting earnings announcements. Additionally, there may come a point where rebuilding a short position in certain equities or indexes becomes warranted.

As you will see in the charts below, I believe the S&P 500 could retest 2022’s lows of 3,500 – if not lower depending on the speed of the market drop.

Looking Forward:

While the stock market continues to show signs of cracking, the bond market is doing the same. Yesterday the Treasury announced they would issue approximately $776 billion of new debt for Q4 2023 and $815 billion for Q1 2024 (both historically records). These amounts are comparable to the issuance in Q3 2023 which catapulted the yield for the 10 year Treasury from 4.06% on August 31st to around 4.9% as of late. This led to bond prices dropping 5-17% (depending on the bond’s maturity) over that period of time.

After reviewing where long term interest rates have traded for the last 40 years there is a strong chance the 10 year Treasury could see a yield between 5.25% and 6% which would lead to additional declines in the bond market. However, there will come a point where bond yields will stabilize warranting a shift from a 5% money market/short term bond strategy to a 5%+ long term bond strategy.

Detailed Analysis:

To better explain the aforementioned summary I am going to provide you with some charts along with an analysis of each chart. The goal is to help you understand some of my concerns related to the macro economic environment.

Let me start off with a concern related to S&P 500 earnings, which directly affects stock market valuations. For the last year I have been tracking the S&P 500’s prior earnings for the last 50 years (see below). You can see earnings have recently trended well above the historic channel as indicated by the light blue lines. The only other time we see a deviation outside of this channel is during the Great Financial Crisis in 2008. While the 2008 deviation went below the channel it eventually returned back to the average as the market and economy improved. This reversion to the mean supports the idea that we could see a decline in S&P 500 earnings due to higher borrowing costs, a deteriorating consumer, excess Treasury issuance to fund the government, and ongoing monetary tightening.

While past performance is no guarantee of future results, if companies start laying off employees and employees start defaulting on their stretched debt then consumer bankruptcies will increase, not to mention they won’t be able to continue purchasing at their prior pace. This will affect various sectors of the market which will lead to earnings compression. Historically speaking, when the economy reaches the trough of a recession the earnings multiple for the S&P 500 can range between 12X to 15X and earnings can decline 16.4% on average, depending on the sector.

In an article written by Schroder’s in August of 2022, when looking at the past 15 recessions over the last 90 years earnings have only bottomed three times during a recession. Furthermore, the average number of months from the bottom of the stock market to the trough in earnings is eight months. Therefore, there is a high probability the market will decline before earnings bottom in 2024.

Based on a projected 2023 S&P 500 earnings of 225 this could mean S&P earnings for 2024 could drop to 180 – 200. Using the mid-point of 190 and a multiple of 15X the S&P 500 Market Cap Weighted Index could drop to around 2,850. Based on today’s 10/31/23 close this would result in a 32% decline, which has been the average drawdown during the last 10 recessions.

A decline of that amount is not said “lightly”. The charts below indicate the support for this thesis assuming the various equity markets trade to the bottom of the 10 year trend channel and not below.

Let’s now move on to the charts to help elaborate on the information discussed:

- Sector Performance Year-To-Date

- S&P 500 Earnings For Prior 50 Years

- S&P 500 Earnings For Prior 50 Years (LOG FUNCTION)

- S&P 500 Earnings Yield (Prior 70 Years)

- 10 Year Treasury Historic Chart

- Federal Reserve Bank Charge Offs & Delinquency Rates on Loans and Leases at Commercial Banks

- Federal Reserve M1 & M2 Supply

- Federal Reserve Household Debt Service And Financial Obligations Ratios

- Federal Reserve Household Balance Sheets

- Federal Reserve Household Balance Sheets As A Percentage Of Disposable Personal Income

- Federal Reserve Household Credit Card Debt

- Federal Reserve Debt Breakdown

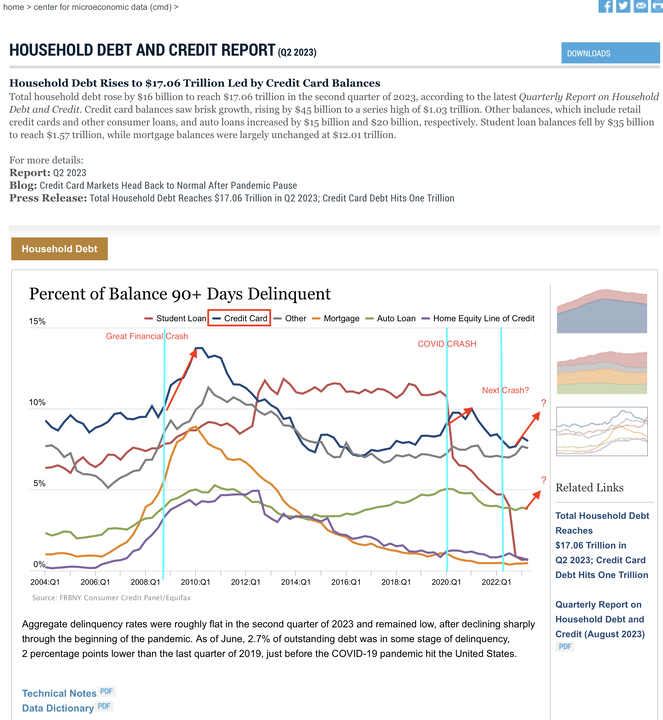

- Federal Reserve 90 Day Delinquency Rates

- US Core Inflation Rate

- Nasdaq 10 YR Chart 1993 – 2002

- Nasdaq 10 YR Chart 2015 – 2025

- S&P 500 10 YR Chart 1993 – 2002

- S&P 500 10 YR Chart 2015 – 2025

- S&P 500 Equal Weight 10YR Chart

- Small Cap 10YR Chart

- Semiconductor 10YR Chart

To help you navigate the charts I have marked the charts with some key points to consider. Since there are a lot of technical indicators in each chart I will explain some of the indicators I am watching. Should you want to discuss any or all charts in greater detail click the button below to book a Portfolio Review.

S&P 500 Earnings (Charts 2 – 4):

The first chart reflects the S&P 500 earnings over the past 50 years. The dark blue line has oscillated in a range, or up-trend channel (illustrated by the light blue lines). The two times the earnings varied outside this channel were during the Great Recession of 2008 and again between 2021 to 2023. The first time earnings fell below the channel while the second time earnings went well above the channel. This means for earnings to return to the average today’s earnings need to decline.

The second chart is an illustration of the first chart but in a log format. Log functions smooth out curves in statistical data. As illustrated in this graph, earnings have fluctuated between an upper bound (the light blue line) and a lower bound (the red line). Unlike the first chart, earnings have fluctuated between these ranges for the entire 50 years, with the exception of the Great Recession (which should highlight how severe that decline was). This chart indicates earnings are hovering at the top end of the 50 year range.

The third chart is of the S&P 500 earnings yield for the last 70 years. As of last week the S&P 500’s earnings yield traded one standard deviation below its historic average. Every time the stock market declined the earnings yield increased. When this happens investors tend to view the stock market as more attractive for long term investment. If the earnings yield hovers around 1.6% and the 10 year Treasury pays close to 4.85%… investors are currently more incentivized to lock money away in money markets or bonds.

10 Year Treasury Chart:

Turning our attention to the 10 Year Treasury yield it is important to note rates currently sit at almost 15 year highs. Between 2006 and 2007 the 10 year Treasury peaked around 5.15% Today we continue to bump up against 5%.

Unfortunately, with the Treasury’s issuance of new debt at all-time highs there is a strong probability that 10 year bond yields will continue to climb. Based on past trends it is my opinion that the 10 year Treasury will push above 5% and move toward 5.25%, with a possibility of even reaching 6%.

Should the 10 year Treasury move closer to 5.25% or even 6% it is possible that 30 year mortgage rates could approach 9% – 9.5% as these two rates are indirectly linked. If this were to happen the entire bond market would continue to reprice and move downward. Only a significant flight to safety could put downward pressure on long term yields allowing long term yields to remain lower than estimates.

If the 10 year Treasury moves closer to 5.25% – 6% then an investor may want to consider moving money from money market and short term bonds into longer term bonds. This way an investor can continue to collect higher yields AND the opportunity for capital appreciation when the Federal Reserve eventually cuts interest rates.

Federal Reserve Charts (Charts 6 – 13):

I provided the Federal Reserve charts as a means to understand the health of the economy today.

The first chart shows how delinquency rates have started to increase over the last few quarters, trending toward 2021’s highs. Should we enter a recession, as seen in 2008, delinquency rates will continue to increase – possibly returning to 2008 levels.

The second chart illustrates how M1 & M2 money supply has declined over the past year. Dusting off the economic degree, this is the amount of money (liquid cash) residing in the US economy today. The chart shows money supply has declined significantly over the past year and continues to decline as previously issued bonds mature AND interest rates remain higher for longer.

The next six charts showcase debt is higher than 10 years ago, consumer balance sheets are weak, and 90 day delinquencies are increasing.

US Core Inflation Rate:

While core inflation continues to decline the rate continues to be stubbornly high. To reach the Federal Reserve’s 2% inflation target economic growth needs to sufficiently slow down. With Q3 2023 GDP reported at 4.9% and Chair Powell’s comments about wanting below trend growth, core inflation needs to decline at a more rapid pace.

To accomplish lower inflation the Board of Governor’s needs to either continue increasing interest rates OR keep interest rates higher for longer than normal. However, in either case if the Federal Reserve delays rate cuts into a recession stock prices could decline steeper, as indicated in the Schroder’s article.

Nasdaq 10 Year Chart:

For the last year I have been sending charts of the Nasdaq to clients as a way to show how it has traded above the prior 10 year trend. My biggest concern has been how overvalued it has been for the last three years. To help draw a comparison between the DotCom bubble, and corresponding economy growth, to our current situation I have provided two charts.

The first chart reflects the price action between 1993 and 2002. The second chart reflects 2015 to what could be in 2025. In both charts I have illustrated a channel where stock prices traded within a range, until they didn’t. In the final few years of the channel you can see the Nasdaq exceeded the channel by A LOT. This above trend growth eventually reverted to the mean between 2000 and 2002.

Unlike the DotCom bubble, 2023 saw a rally in 10 stocks (making up nearly 50% of the index) which drove the stock market up – almost to the point where it peaked in 2021. This would have almost reset the decline from 2022 making a future decline all that much more steep.

S&P 500 Market Weighted Chart:

Similar to the Nasdaq chart, the S&P 500 Market Cap Weighted index is challenged. With 10 stocks making up nearly 30% of the index, the index has pushed higher because of these stocks. When comparing the 1993 to 2002 chart to 2015 to 2025 chart there is a much bigger concern now than 30 years ago.

Thirty years ago the price action remained in the channel until the Nasdaq broke down. Since technology was a component of the S&P 500 back then the Nasdaq’s decline weighed on the S&P 500.

Looking at today’s chart we can see the S&P 500 has traded well above the previous trend line, most likely due to the high concentration in 10 stocks. This poses a big concern when looking ahead.

If the consumer’s health is declining then the economy’s health will continue to deteriorate. If the economy deteriorates it will be due to corporate revenues and profits declining. When profits decline Earnings Per Share will decline which will affect stock valuations.

S&P 500 Equal Weighted Chart:

Unlike the Market Cap Weighted S&P, this index tries to smooth out the edges by not holding high concentrations to any one of the 11 sectors in the market. However, even with that this chart highlights two periods where the index traded outside of its 10 year channel. The first time was during the COVID crash and the second time was shortly after.

If the COVID crash dropped below the channel then the reversion to the mean would mean the index would need to trade up to the average. To the same end, the current index price action would mean the index needs to fall reach the “average”.

This chart would potentially indicate this index could drop 10-12% from current levels. If that were to happen the Market Cap Weighted S&P 500 could drop 16% – 20% from current levels.

Russell 2000 Small Cap Chart:

This index has been very hard to read over the last year. This chart has been trading within its 10 year trend channel. In fact, when comparing large cap stocks to small cap stocks… small cap stocks look more attractive to invest in. This is why I have been focused on capturing a potential bounce in this part of the equity market… that is until recently.

If a year-end rally is looking bleak and a large market decline looks more likely then it would be hard to believe small cap stocks would make a rally – especially when borrowing costs due to higher interest rates will affect this group of stocks more than large cap stocks.

It is my opinion that this index could eventually trade below its 10 year trend channel like it did during the COVID crash. Should this happen this index will be massively undervalued and present an opportunity to capture a rebound – especially since small cap stocks tend to lead a recovery market.

SemiConductor Charts:

I wanted to include this index as it was the main culprit to driving the 2023 market explosion. In fact, the chart shows that this index peaked in July 2023 almost 5% below the 2021 highs. If the economy declines the need for semiconductors should decline (e.g. chips for computers, chips for cars, and chips for data servers).

If the Nasdaq declines so does the Semiconductor Index because six of the top 25 stocks in the Nasdaq make up six of the top 10 stocks in the Semiconductor Index.

In the end, I continue to worry about the market – like I have said all year long. The equity markets shouldn’t have rallied in 2023 the way they did. US equity markets should be lower that where they trade now. Today I am focused on reducing volatility in your portfolio with a defensive strategy.

To discuss our investment thesis, our outlook, and your portfolio in greater detail please click the link below and schedule a time that works with your calendar.